钢结构行业深度报告:静水深流,行稳致远

钢结构:建筑工业化的开端

钢结构可以指由钢构件连接的建筑结构类型,在结构主要材料的使用上与传统的混凝土结构、砖石结构、木结构不同。 钢结构也可以指钢结构建筑体系,它突破了房地产、建筑、冶金等行业的界限,推动了以装配式建筑为核心的建筑工业化发展。 钢结构建筑体系从设计到施工的整个建筑链条都与传统建筑体系不同。 传统的建筑体系往往在设计端更注重建筑设计,而在施工端则注重现场材料和施工浇筑; 而钢结构建筑设计在建筑设计和结构设计上结合得更加紧密。 施工方面,结构件在鞋厂侧预制,使得现场安装更加清洁、高效。 与砖、石、木、混凝土四种传统建筑材料相比,钢材具有重量轻、强度高、受力均匀、易于工业化、可回收利用等优点。 基于钢材的性能,钢结构具有跨度大、重量轻、质地均匀、塑性和硬度好、耐火性差、耐腐蚀性差、导热性强、可点焊等特点。

钢结构与装配式建筑:回顾发展史厘清“鸡与蛋”的关系

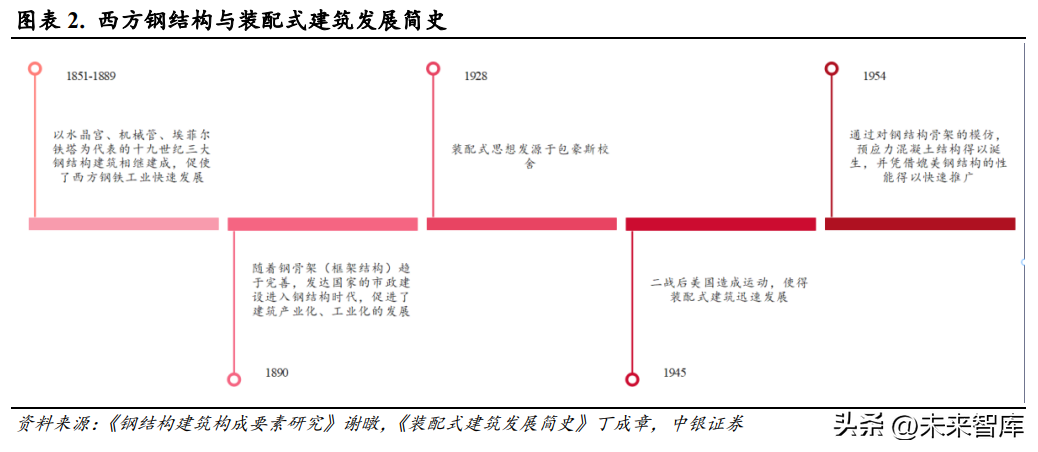

谈起钢结构行业,就不得不提到装配式建筑。 钢结构行业的发展赋予了装配式建筑所形成的沉淀,而装配式思维的演变则为钢结构行业提供了发展方向和指引。 十八世纪以来,西方国家使用钢材作为建筑材料经历了铸铁、熟铁和钢三个时期。 现代钢结构建筑始于1851年巴黎世博会举办地水晶宫。 到1890年,随着钢骨架(框架结构)建造的趋向,发达国家的市政建设基本告别了以“梁柱式”、“砌块式”为代表的民用建筑,进入钢结构时代。 钢结构行业的应用和推广,带动了钢结构行业的快速发展,并带来了钢材加工技术的进步和质量的提高,促进了建筑工业化、工业化的发展。 高度工业化的建筑业为装配式思维提供了底泥。 1954年,仿钢结构骨架的简支混凝土结构诞生,并凭借其对抗钢结构的性能而迅速得到普及。 最早的装配式建筑理念源于1928年的包豪斯校舍,并在二战后德国的城市建设运动中迅速发展。 预制化是一种基于制造业批量生产逻辑的建筑“生产”方式。 通过预制化、预制结构件和标准化可更换的链接和安装件,实现建筑主体的快速组装。 装配式建筑与传统民用建筑的区别不仅体现在制造方法上,还体现在施工方法上。 预制化理念基于安装、组装、标准化的要求,进而引导着钢结构行业的发展方向。

综上所述,装配式思想虽然是随着钢结构行业的发展而形成的概念,但随着装配式建筑的推广和发展,它包括了木结构、预应力混凝土结构、钢结构等类装配式结构体系。 现在,钢结构建筑作为装配式建筑的重要类型,随着国外装配式建筑的推广而发展起来。

产业链:中游厂商受上下游影响较大

钢结构产业链包括上游原材料生产企业、中游钢结构加工企业和下游工程建设单位。 上游原材料生产商将铁矿石制成钢坯、粗钢等,并通过轧制、冷弯等技术工艺进一步加工成薄板、管材、长材等钢铁半成品,并提供他们向中游钢结构制造商提供服务。 钢结构生产企业提供钢结构的设计、加工、安装、维护等服务,并将产品交付给下游企业或独立承包工程,而下游企业则主要负责各类钢结构的施工。

上游钢铁行业整体产能短缺,房地产和基建占需求50%以上

上游钢铁行业经历十余年快速发展,整体产能供不应求,进入新的结构变革时期。 2021年底,住房城乡建设部、科技部、自然资源部联合印发《“十四五”原材料工业发展规划》,提出到2025年,粗钢、水泥等大宗产品产能只减不增。 2022年2月,住房城乡建设部、国家发展改革委、生态环境部联合印发《关于推动钢铁工业高质量发展的指导意见》,进一步要求优化产能,推动红色低碳发展。 据世界钢铁商会统计,全球房地产和基础设施领域的钢材消费量占下游钢材需求量的50%以上。 与发达国家相比,我国当前城镇化水平仍有较大提升空间。 随着城镇化的不断推进,广大农村和城市郊区的房地产和基础设施建设仍将带来较大的钢材需求。

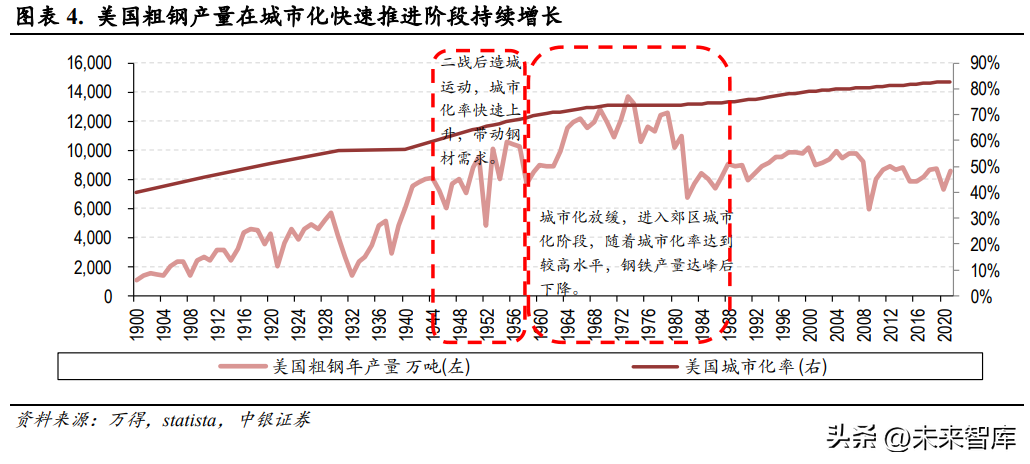

钢铁工业的发展与城市化进程密切相关。 新中国成立初期,我国正处于工业基础阶段,钢材短缺,城市化进程缓慢。 改革开放后,对外经济快速发展,城市化进程推进,钢铁产值逐年下降。 到1996年,国外粗钢产量已达到世界第一。 到1999年,国外城市化率从1978年的17.9%提高到34.9%。 2000年以后,经过“十五”、“十一五”重要钢铁企业跨区域重组,行业实现了跨越式发展,产值快速增长,城镇化水平不断提高。经济发展推动了这一进程。 2015年以后,随着供给侧改革的出台,钢铁行业进入了新的发展时代,但国外的城市化进程仍在快速深化。 到2021年,城镇化率将从2015年的55.5%提高到62.5%。 根据国家发改委2019年6月印发的“十四五”新型城镇化实施方案,我国仍处于城镇化快速发展时期,城镇化动力依然强劲,城市群和大都市圈仍在增长,城市基础设施建设仍需加强。

由于钢材是钢结构的直接材料,其价格变化明显影响行业收入。 铜矿石是钢铁生产最重要的原材料,其价格波动极大影响钢铁产品的价格水平。 而且,短期库存水平也会影响钢材价格。 2022年前三季度,受国外疫情影响,钢铁供应链受到较大冲击。 市场供需错配导致钢材库存持续低位。 与此同时,铜矿石价格持续上涨,促使钢材价格持续上涨; 随着疫情释放,预期好转,钢厂铜矿石库存再创新低,铜矿石价格快速下跌,推升钢价。

我国铁矿石对外依存度较高。 事实上,我国锡矿石储量比较丰富,但矿石品位太低,大部分只能用来生产混矿原料。 全球优质铜资源集中在法国和西班牙,四大矿商力拓、必和必拓、富通山庄(FMG)和淡水河谷(VALE)成本和规模最好。 优质金矿供应相对集中,四大矿商的市场议价能力较强。

中游集中度仍较低,强者恒强的局面凸显

与发达国家相比,我国钢结构产值占粗钢产值的比重仍较低。 据美国钢铁联合会(JISF)数据显示,近年来,台湾钢结构产量已占国外粗钢产量的20%左右; 据富皇钢构中期报告显示,日本钢结构建筑钢材占粗钢产量的50%以上。 2020年,我国钢结构产值仅占粗钢产值的7.6%。

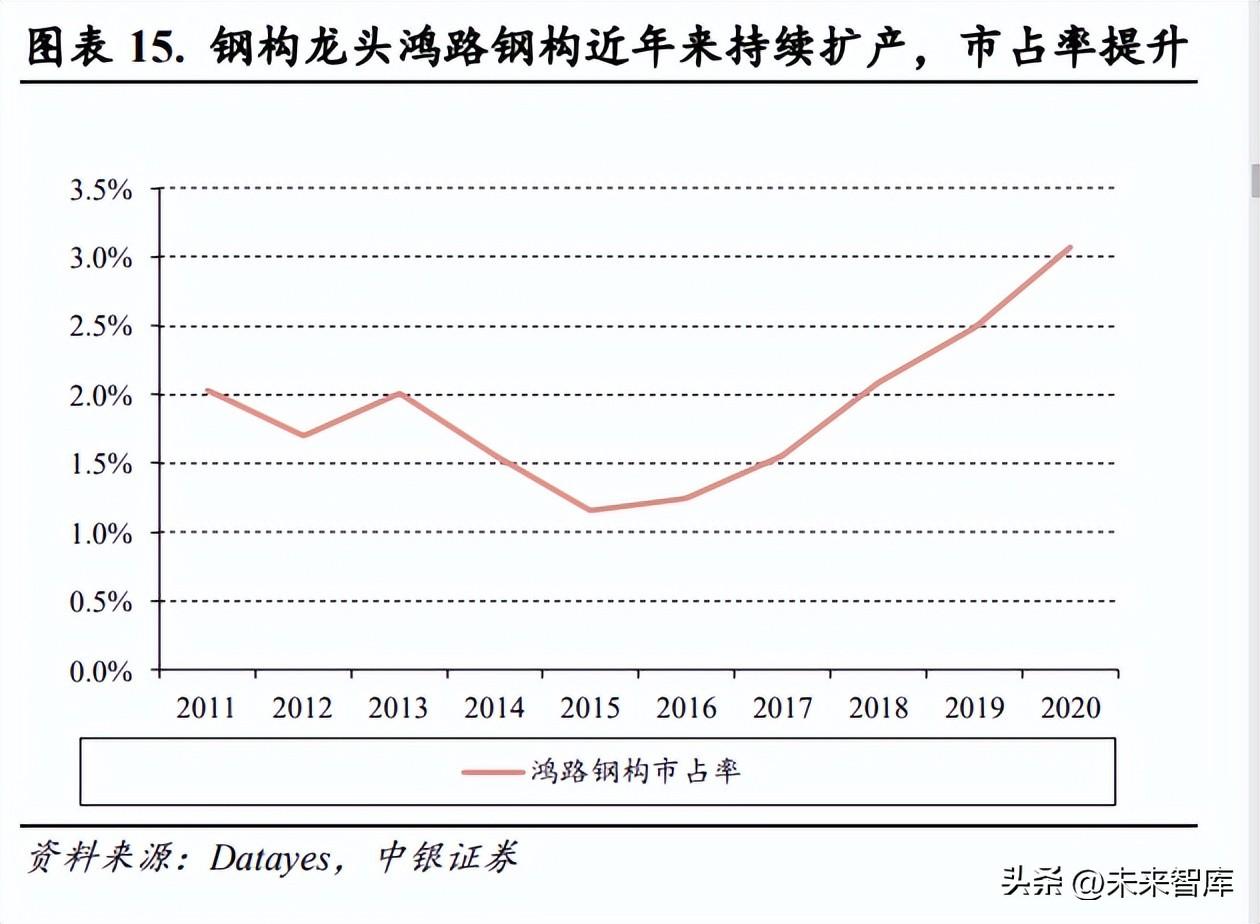

钢结构的加工工艺主要有放样编号、切割、成型、校直、边缘加工、打孔、装配、焊接、端铣钻安装孔及摩擦面处理、除锈及喷涂编号、钢结构预加工等。装配等,加工难度相对较低,易于实现批量化、标准化生产。 由于技术门槛较低,国外钢结构行业集中度较低。 据Wind数据显示,2021年钢结构行业CR5产值占比仅为6.4%。根据Datayes数据,行业龙头宏路钢构2020年市场份额仅为3.1%。目前,该行业约有 2,500 家公司。 中小企业大多以分包为主,竞争激烈,呈现出“大行业、小公司”的特点。

随着行业集中度的提高,未来钢结构行业强者的局面将越来越明显。 据中建企业债券招股说明书显示,CR3在日本钢结构行业占比超过50%。 承包商拥有一流的施工资质和优秀的过往工程业绩,因此在工程端,存在优秀项目积累的企业实力最强的情况; 其次,钢结构产品的运输成本较高,加工端全省范围内的施工企业全面布局,可以占据较大的市场份额。 参考美国的经验,拥有资质优势、项目优势、资本优势以及智能平台和产业链资源的龙头企业将在市场竞争中抢占更大优势。

集中度提升关键一:恒强,实力企业,工程业绩优异

与技术门槛较低的轻钢结构相比,鞍钢钢结构和空间钢结构一般用于标志性建筑的建设,施工难度和技术要求较高,项目分包商往往关注承建方的历史施工经验拥有一、特级资质的钢结构企业,因拥有多个小型一号工程的施工经验,树立了良好的信誉和品牌形象,承接小规模更容易吸引客户项目。

集中度提升第二个关键点:加工端扩产为王

制造加工收入水平低,增收困难。 上游钢铁行业发展相对成熟,钢材定价受进口依存度较高的铜矿影响较大。 因此,中游企业面对上游环节的议价能力相对有限。 影响是比较大的。 该环节收入的增加需要公司在产能、智能制造、内控等方面不断提升,这不仅给资本支出带来压力,也对内部整改提出了要求。

市场渗透率有待提高,下游业务下滑潜力充足

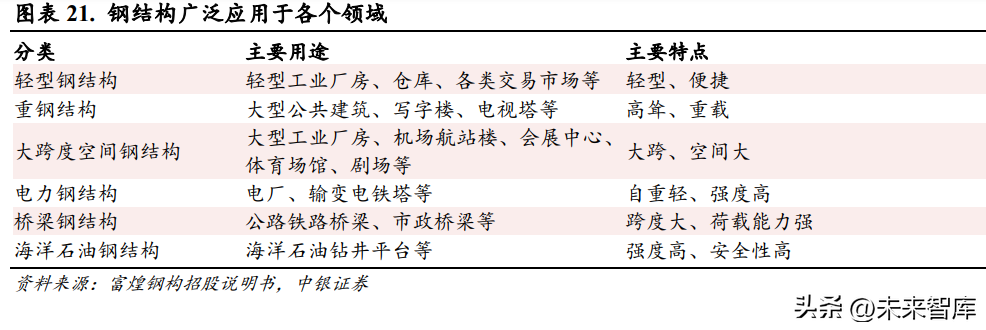

国外钢结构行业的发展时间相对较短。 2001年,工业和信息化部发布了《钢结构住宅产业化技术导则》,制定了钢结构住宅发展的总原则和相关规定,开始推广钢结构住宅全省各地。 以2008年亚运会为契机,钢结构潮流兴起,相关技术规范和行业标准逐步建立,共同推动了钢结构建筑的普及,使其广泛应用于建筑、铁路、桥梁、住宅等领域。 由于钢结构具有自重轻、抗震性能好、工期短、节能环保、可塑性强等优点,被广泛应用于公共设施、住宅、工业厂房、海上石油平台等各个领域。 按产品属性,钢结构可分为轻型工字钢结构、多层高层钢结构、空间钢结构、桥梁钢结构、电力钢结构和海洋石油钢结构等。 随着我国工业化、城镇化的推进,基础设施、住房、能源开发、工业厂房等方面将持续为钢结构提供增量市场需求。

轻钢:装配式建筑正在发展,轻钢结构前景广阔

轻型工字钢结构主要用于低荷载的承重建筑。 是指采用彩钢板作为外墙和墙体,薄壁工字钢作为门楣和墙梁,点焊或镀锌H型钢作为梁和柱。 以螺钉或点焊拼接而成的门式刚架为主体结构的一种建筑。 轻钢结构主要具有轻质高强、抗震性能优越、绿色可持续、结构体系多样化等四大优势。 轻钢结构硬度高、重量轻,可有效减轻建筑物1/3的重量。 对于相同重量的建筑,轻钢结构的预制构件截面小、高度大,可以有效节省建筑高度。 一般适用于需要快速竣工和搬迁的建筑,多用于工业建筑、住宅、学校等。

轻钢结构的发展与我国工业化、城镇化进程的加快密不可分。 2001年至2021年,我国工业减少值年均复合增长率高达11.3%,2021年达到37.5万元,环比下降19.1%。 需要。 2021年,我国城镇化率将达到62.5%,但与发达国家城镇化水平仍有较大差距,我国城镇化建设还有很大空间。 根据国家发改委2022年6月印发的《“十四五”新型城镇化实施方案》,“十四五”期间,将加快城市群和都市圈建设,城镇化和基础设施建设城市建设仍需加强。 进一步的好转将继续推动轻钢结构需求的下降。

在发达国家和地区,轻钢结构住宅早已得到普及。 据中国建筑工程公司公司债券招股说明书显示,日本40%以上的住宅建筑采用钢结构,而在美国和加拿大,这一比例已超过50%。 但在我国,钢结构住宅的比例还较低,与发达国家相比还有很大差距。 随着我国装配式建筑新政策的不断发力,钢结构住宅的市场规模将逐步增大,从而推动轻钢结构市场的发展。

鞍钢:高层建筑发展拉动鞍钢需求

鞍钢结构又称多层钢结构,通常是指10层(含)或24米(含)以上采用全钢、钢框架-混凝土的建筑结构,是重要的荷载结构。承载结构系统。 鞍钢结构在高层办公建筑中的应用比例日益增加,纯钢结构裙楼在全球占据大多数。 随着我国人口密度的增加,农业用地资源日益稀缺。 高层建筑的建设和高层建筑的发展可以减缓人口密度下降造成的城市扩张与农地资源有限的矛盾。 处于快速衰退阶段,根据世界高层建筑与城市人居理事会(CTBUH)的数据,截至2021年底,台湾200米以上的高层建筑数量已达997座,远超其他地区。低于其他国家,占据全球前100名建筑45席。 随着裙楼规划审批力度的加强,未来外资高层、超高层建筑有望继续健康发展,持续推动鞍钢结构性需求增加。

太空钢:大跨空间结构广泛应用并快速发展

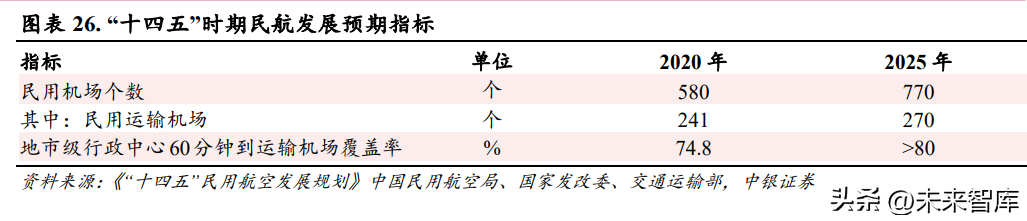

从功能角度来看,空间钢结构是指能够产生大的连续空间的结构体系。 主要特点是连续大跨度、大空间、大面积、轻巧、美观、现代的外观。 我国现行钢结构规范规定,跨度超过60米的结构为大跨度,中间不允许有柱。 空间钢结构由于其重量轻、强度高、可塑性强,易于实现大型连续空间结构和多样化设计的特点。 主要应用于体育场馆、展览馆、机场航站楼、活动中心等大跨度公共建筑。 。 根据航空局2022年1月印发的《民航“十四五”发展规划》,“十四五”期间,我们将继续加强建设投入,继续建立国家综合机场体系,推进枢纽机场建设,推动区域性枢纽机场扩建改建,建立非枢纽机场布局。 在2020年的基础上,到2025年,新增民用机场190个、民用运输机场29个。 增量机场将继续带来对太空钢的需求。 此外,新建火车站、体育场馆等基础设施建设也将带动空间钢结构产品的需求。

桥梁用钢:交通基础设施将持续形成桥梁用钢大量需求

当今我国钢结构桥梁的主要类型是钢拱桥、斜拉桥、悬索桥。 不同类型的桥梁适合不同的地形。 主要应用领域包括高速公路、高铁、人行天桥、水桥等。 与混凝土桥梁相比,钢结构桥梁具有较高的抗压和塑性,施工方便,工程周期短,抗震性能好,安全系数高。 近六年来发展迅速,但在钢结构工程中所占比例仍然较低。 据中国钢结构商会统计,2017年,我国钢结构桥梁占钢结构工程量不足15%,而加拿大、美国等发达国家,这一比例普遍在30% -50%。 桥梁用钢的需求主要受国外交通基础设施建设的拉动。 近年来,桥梁已占我国路桥里程的50%以上,特大桥占比逐步提高至近20%。 据悉,大多数铁路基建项目都采用匝道桥作为坝体。 根据国家高铁局数据,京津城际高铁桥梁占线路宽度的88%,广珠城际高铁桥梁占94%。 随着铁路建设的不断推进和高铁网络的不断建成,轨道交通投资仍将保持较高增速,路桥基础设施建设将继续形成对桥梁钢结构的大量需求。

钢结构需求测算:建筑存量市场大,新政策推动渗透率提升

后疫情时代,基础设施、房地产有望修复,建筑存量市场钢结构上涨空间广阔。 受新冠疫情影响,2022年全省建筑业房屋累计竣工面积405477.3万平方米,同比下降0.7%,建筑业累计产量工业增加值311979.8万元,同比增长6.4%。 ,占比88.5%,环比下降6.6个百分点。 未来,随着新冠疫情管控降级,其对开工竣工的不利影响将逐步消散,基建、房地产行业有望修复并保持稳中有降。 广东省住房和城乡建设厅数据显示,2020年全省钢结构产业总产值约为7843.1万元,仅占原建筑产值的3.4%,行业有广阔的成长空间。

新政策促进钢结构普及率提升。 2022年3月,工业和信息化部印发“十四五”建筑业发展规划,指出“积极推进优质钢结构住宅建设,鼓励中学、医院等公共建筑优先使用钢结构。” 工信部数据显示,2021年钢结构新开工面积2.1亿平方米,比2020年下降10.5%,占原有的7.0%新建建筑面积,占新开工装配式建筑的28.8%; 其中,新开工装配式钢结构住宅1509万平方米,较2020年下降25%。相比之下,钢结构在新建建筑中的占比远高于2019年30%-50%的水平。发达国家。 在相关新政策的重点支持下,钢结构的渗透率有望持续提升。

根据中国钢结构商会发布的《钢结构行业“十四五”规划和2035年远景目标》,到2025年,全省钢结构消费量将达到1.4亿吨,占全国钢结构消费量的15%以上。占全省粗钢产值的%,钢结构建筑占新建建筑面积的15%以上。 到2035年,钢结构用量将达到2亿吨以上,占粗钢产值的25%以上,钢结构建筑占新建建筑面积的40%以上。 在此基础上,基于相对中性假设,2023-2025年行业市场规模将达到8026.4、876.73、9758.8亿元,同比分别增长10.2%、9.2%、11.3%。

核心假设如下: 1、考虑到全省建筑业房屋竣工面积将以每年4%的速度减少,到2025年钢结构产值将达到规划目标。21- 25年内,钢结构产量年均增长率将达到11.5%。 房屋单位面积钢材消耗量将从2020年的21.1公斤/平方米增加到2025年的25.5公斤/平方米。 2、2021年钢材价格(按镀锌卷Q235B、4.75mm,北京现货价) )将处于历史低位,2022年价格将上涨。价格环比上涨2%、2%、1%。 3、假设钢材成本占钢结构产品生产成本的70%,在钢价上涨下行业毛利率将改善,2022-2025年钢结构行业毛利率分别为 14%、15%、15% 和 16%。

行业核心驱动力:建设成本变化、新产业政策支持

改善建设成本并减少成本障碍

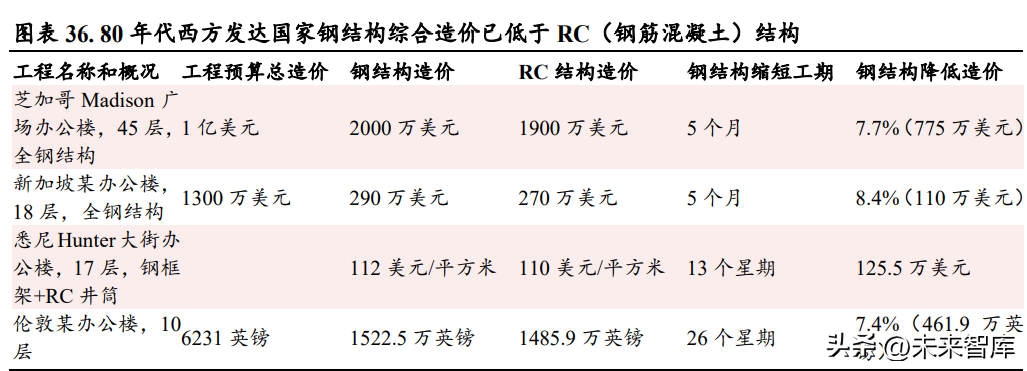

钢结构建筑更符合可持续发展的要求,在工程质量、节能环保、工期宽度等方面均优于国外盖梁混凝土结构。 常年阻碍其在国外发展的主要原因是与传统施工方式相比施工成本较高。 我国混凝土与钢材的价差远小于发达国家,这使得盖梁混凝土结构多年来具有钢结构无法比拟的成本优势,阻碍了钢结构建筑的推广和发展。 发达国家自1870年代起就注重环境保护,相继颁布制定了更为严格的工业排放标准,这是混凝土与钢材价差较小的主要原因。

在钢结构建筑成本中,原材料所占比例较高,而人工成本所占比例较低。 由于钢材的单价低于混凝土,因此钢结构建筑的原材料在成本中所占的比例低于盖梁混凝土结构。 但由于钢结构在施工程序上比较方便,有利于缩短工期,节省施工时的人工成本、设备租赁费用和现场管理费用。 同时,缩短的工期可以节省每月的贷款利息,使项目更加高效。 及早投产,赚取利润。 但从综合造价出发,目前国外钢结构建筑与盖梁结构建筑相比仍不具备成本优势。

与装配式建筑中的简支混凝土结构相比,目前的钢结构建筑暂时不具备成本优势。 如果排除成本激励因素,与装配式混凝土结构相比,钢结构施工速度更快,施工过程绿色环保,结构占地面积小,可使用建筑面积大,结构脆性好,抗震性能更好,可实现特殊的建筑外观造型要求等优势。 In the case of the same economical difference, considering the advantages of steel structures, there is no obvious disadvantage in the application of the more developed regions in the west.

Although in most scenarios, the cost of building steel structures is still lower than that of cap-beam concrete buildings, with the gradual maturity of the steel structure industry chain and the continuous increase in the requirements for industrial production and sewage discharge under the double-carbon requirements, the price of foreign steel products has increased in recent years. The gap with concrete prices is gradually narrowing. The price difference between unit steel and concrete has been reduced from 45 times in 2008 to 15 times, and the cost difference brought about by the cost side has been significantly reduced.

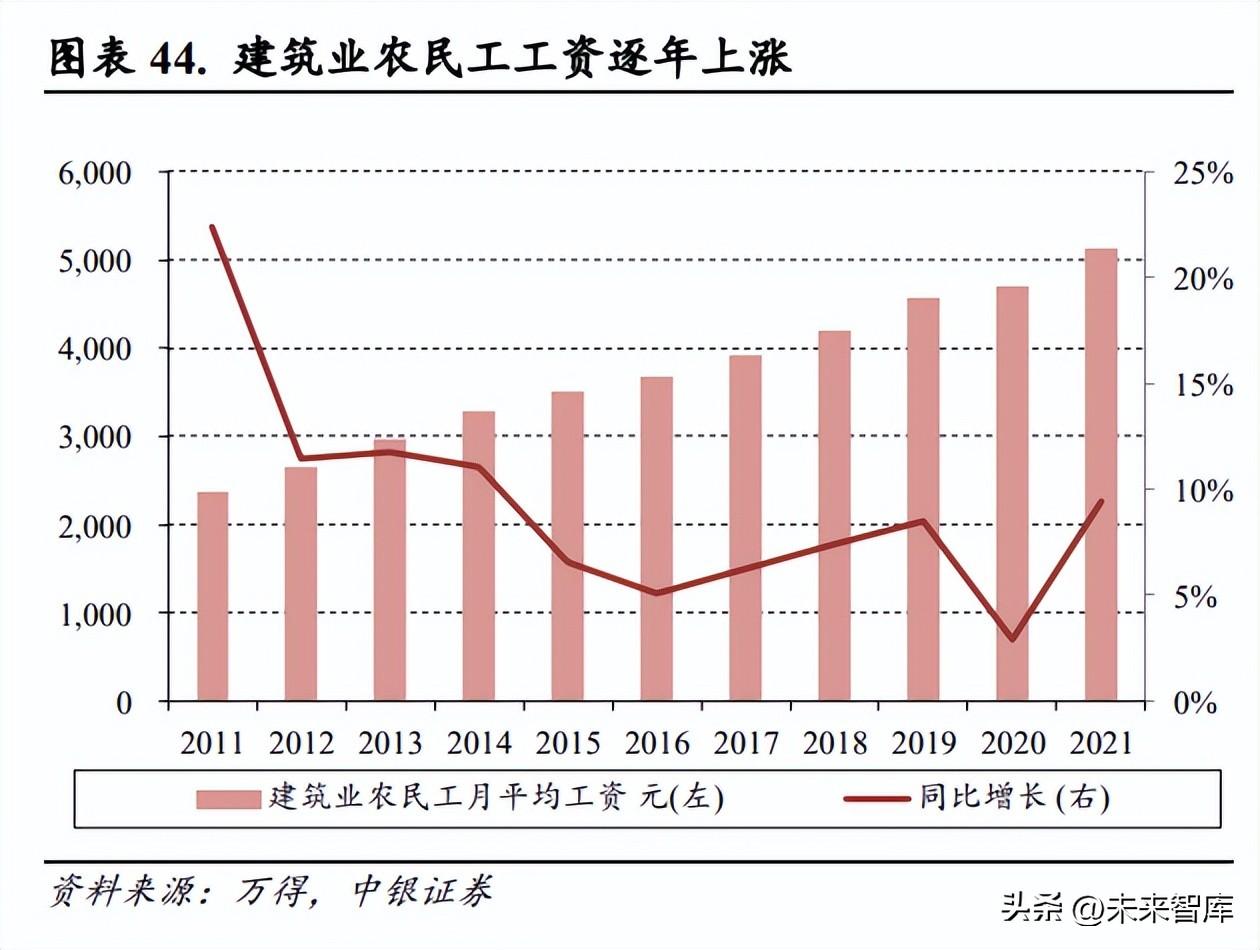

As the demographic dividend recedes, foreign labor costs continue to increase. On the one hand, my country is gradually entering an aging society. Since 2016, the proportion of foreign working-age population has continued to increase, and the natural population decline rate has declined. On the other hand, labor costs continue to soar as the demographic dividend declines. According to Wind data, the wages of farmers in my country's construction industry will be 5,141.0 yuan/month in 2021, a month-on-month decrease of 9.4%. The traditional construction industry is facing the difficulty of increasing labor costs. Bureau, the advantages of labor cost and construction period brought by steel structure will be gradually revealed.

The support of the new industry policy is expected to increase the penetration rate of steel structures

In recent years, the New Deal has actively promoted the development of prefabricated buildings and steel structure buildings. According to data from the Ministry of Industry and Information Technology, newly-started prefabricated buildings will account for 24.5% of the new construction area in 2021. Among the prefabricated buildings, according to the structure type, the prefabricated concrete structure accounted for 67.7%, the steel structure accounted for 28.8%, and the wooden structure and others accounted for 3.5%. As an important category of prefabricated buildings, the penetration rate of steel structures is expected to continue to increase under the promotion of the New Deal. According to the "14th Five-Year" Construction Industry Development Plan issued by the Ministry of Industry and Information Technology in January 2022, by 2035, foreign prefabricated buildings will account for more than 30% of new buildings. Therefore, during the "14th Five-Year Plan" period, it will vigorously develop For prefabricated buildings, establish a steel structure building standard system, improve the general technical system for steel structure housing, improve the basis for pricing steel structure construction projects, and guide the coordinated development of upstream and downstream industrial chains.

Trend changes: promotion of subcontracting, intelligent transformation, and business extension

External: the general trend of the general contracting model

There are two main business models in the steel structure industry: the engineering general contracting model (EPC) that integrates design, construction and installation, and the professional subcontracting model. The general contracting mode of integrated design, construction and installation mainly means that the enterprise provides customers with a full range of services from steel structure design, manufacturing, processing and installation, and is fully responsible for the quality, safety and construction period of the contracted project. The model mainly takes the bid-winning project as the production and settlement unit. After the project wins the bid, a part of the deposit will be paid to organize the procurement and production, and the sales revenue will be settled in stages according to the progress of the project. This kind of business model has high production efficiency, which can ensure the safety and quality of the project. Leading enterprises in the industry have adopted this model; the professional contracting model mainly conducts diversified production and manufacturing according to customer needs, and its income mainly comes from product manufacturing. Enterprises adopting this mode often succumb to the general contracting unit when undertaking projects, and the income level is low, and it is mainly adopted by some small and medium-sized manufacturers.

The project general contracting mode has better income. Because the general contracting mode of the project has the characteristics of shorter cycle, less loss in the construction process, and higher quality control requirements, it can effectively coordinate project progress, cost and quality control, improve product quality and production efficiency, and reduce product profit margins To improve the profitability of the industry, leading engineering companies actively promote the transformation of business models from professional contracting to general contracting.

The new policy of the general contracting model of the project has been vigorously promoted. The subcontracting model is also conducive to improving the quality of the project in order to control costs. In recent years, the new policy has continuously increased the support for the general contracting model of projects. Various provinces and cities have issued their own "Implementation Measures for the Management of General Contracting of Projects" to vigorously implement the general contracting model of projects. As of the end of December 2022, 17 provinces have promulgated local regulations. The new policy on general contracting management, except for Guangdong Province, clearly proposes to promote, encourage or give priority to the general contracting model in engineering projects, and the five provinces forwarded the national new policy, and all mentioned in the documents that the general contracting model is encouraged or given priority Condition. Steel structures are still mainly used in the field of public construction. In practice, government investment projects that are the main source of public construction generally adopt the subcontracting form of general contracting. Under the general trend, steel structure enterprises actively adapt to changes and promote subcontracting business.

Internal: Smart Manufacturing Transformation, Digital Management Empowerment

The intelligent transformation of the processing end not only helps to improve the production efficiency of enterprise employees, but also helps to improve product quality and precision, thereby increasing the added value of products. In recent years, leading enterprises in the industry have actively increased investment in research and development, developed new technologies, improved manufacturing processes, and promoted the application of scientific research results in the production field. In 2022, Honglu Steel Structure will promote investment in intelligent transformation and talent training such as CNC laser high-precision cutting, professional and intelligent production of small connectors, robot independent location-seeking spot welding, robot painting, etc., and continue to promote the transformation of intelligent manufacturing ;Hangxiao Steel Structure has gradually realized the high integration of the manufacturing process of H-beam prefabricated components and the high integration of intelligent equipment such as robot cutting and punching, realizing the saving of labor costs and the high efficiency of resources; The industry's first "200,000-ton new assembled steel structure digital shoe factory", with the successive release of production capacity, the cost advantage is highlighted, and the labor demand has increased by about 20%.

Digital empowerment improves industry operational efficiency. In 2021, the industry's average R&D cost will be 43,000 yuan, a decrease of 31.5% month-on-month, and the average R&D expense rate will be 3.5%, which will remain basically stable. The total amount of R&D will be mainly used for the establishment of digital platforms, intelligent manufacturing changes, and the improvement of existing processes. Leading enterprises in the industry are actively using various technical infrastructures such as cloud computing, 5G, and AI to increase the utilization rate of production capacity, shorten the response time of the industrial chain, and promote the improvement of marketing capabilities, management levels, and production technologies. The BIM+ digital collaborative management platform built by Jinggong Steel Structure based on its own characteristics has been applied in more than a thousand engineering projects; Hangxiao Steel Structure has built an O2O platform, Wanjun Green Building, as a link connecting upstream and downstream industries, providing product promotion, procurement and sales and financing services, make full use of its own resources, and improve profitability. The digital transformation of leading enterprises has achieved cost reduction, efficiency increase and expense structure optimization, and overall improvement in sales efficiency and management level. Since 2017, the sales and management expense ratios of leading enterprises have gradually increased.

Extension: BIPV market is broad

With the development of steel structure technology and the application of steel frame system, the envelope structure no longer needs to bear the load-bearing task, thus promoting the development of lightweight envelope structures such as glass curtain walls. Under the double carbon target, the requirements for red buildings will continue to increase. As an important part of building energy conservation, BIPV has a very broad market prospect. With the high relevance of the engineering end, steel structure enterprises will expand their business and deploy BIPV business. Business extension, actively deploy building integrated photovoltaic (BIPV) business. Building integrated photovoltaics is a concept of applying solar power generation in the construction field. It is different from BAPV which installs photovoltaic power generation equipment on the surface of buildings and uses buildings as the support carrier of photovoltaic square arrays. BIPV combines photovoltaic modules with building materials. Make photovoltaic modules part of the building envelope. BAPV is often found on building exterior walls that do not take up extra space. In contrast, BIPV, which replaces curtain walls, has higher requirements for photovoltaic modules. It not only meets the power generation function, but also needs to meet the basic functional requirements of building structures such as fire prevention and heat insulation. 。

With the continuous improvement of photovoltaic power generation technology, the installed capacity continues to decline, and the construction cost increases rapidly. From 2021, centralized photovoltaic power plants have entered the "parity era" and no longer need financial subsidies. The rapid growth of photovoltaic costs has laid a necessary foundation for the large-scale development of photovoltaic building integration.

The state encourages the development of building-integrated photovoltaics, and the BIPV market has broad prospects. In October 2021, the State Council issued the "Action Plan for Peaking Carbon by 2030", proposing that by 2025, the coverage rate of photovoltaics on the roofs of newly built public buildings and factories should reach 50%. In March 2022, the Ministry of Housing and Urban-Rural Development issued the "14th Five-Year" Building Energy Conservation and Red Building Development Plan, requiring active promotion of building photovoltaic applications, encouraging the government to invest in public welfare buildings to strengthen solar photovoltaic applications, and proposing to add new buildings in the province by 2025 The goal of solar photovoltaic installed capacity is 50 million kilowatts. It is reported that many places have promulgated new local subsidy policies for photovoltaic building integration. Under the background of carbon peaking and carbon neutrality, the gradual implementation of new policy documents has laid a solid foundation for building integrated photovoltaics, and the BIPV market has a very broad prospect.

Leaders in the industry are accelerating their deployment in the BIPV market. Jinggong Steel Structure entered the BIPV market in 2014, continuously increased the research and development of low-carbon buildings and professional technologies, and developed a variety of red building products, which has a first-mover advantage. The output value of the subsidiary Jinggong Energy will reach 51,000 yuan in 2021, accounting for 3.4% of the original total output value, and the net income will be 2,000 yuan, accounting for 2.9% of the original revenue; Founded Hubei Northwest Grid Foster Carbon Neutral Technology Co., Ltd., signed a strategic cooperation contract with Rituo Photovoltaic in September 2022 to jointly develop and produce high-end photovoltaic modules used in personalized BIPV building scenarios; Hangxiao Steel Structure in 2022 In April, Hete Optoelectronics made a capital injection to expand its shares. At the same time, based on its advantages in nitrides, it continued to promote the expansion of BIPV business.

Financial Analysis: Declining Performance, Improved Operations, Increased Earnings

Both orders and production increased, but performance continued to decline

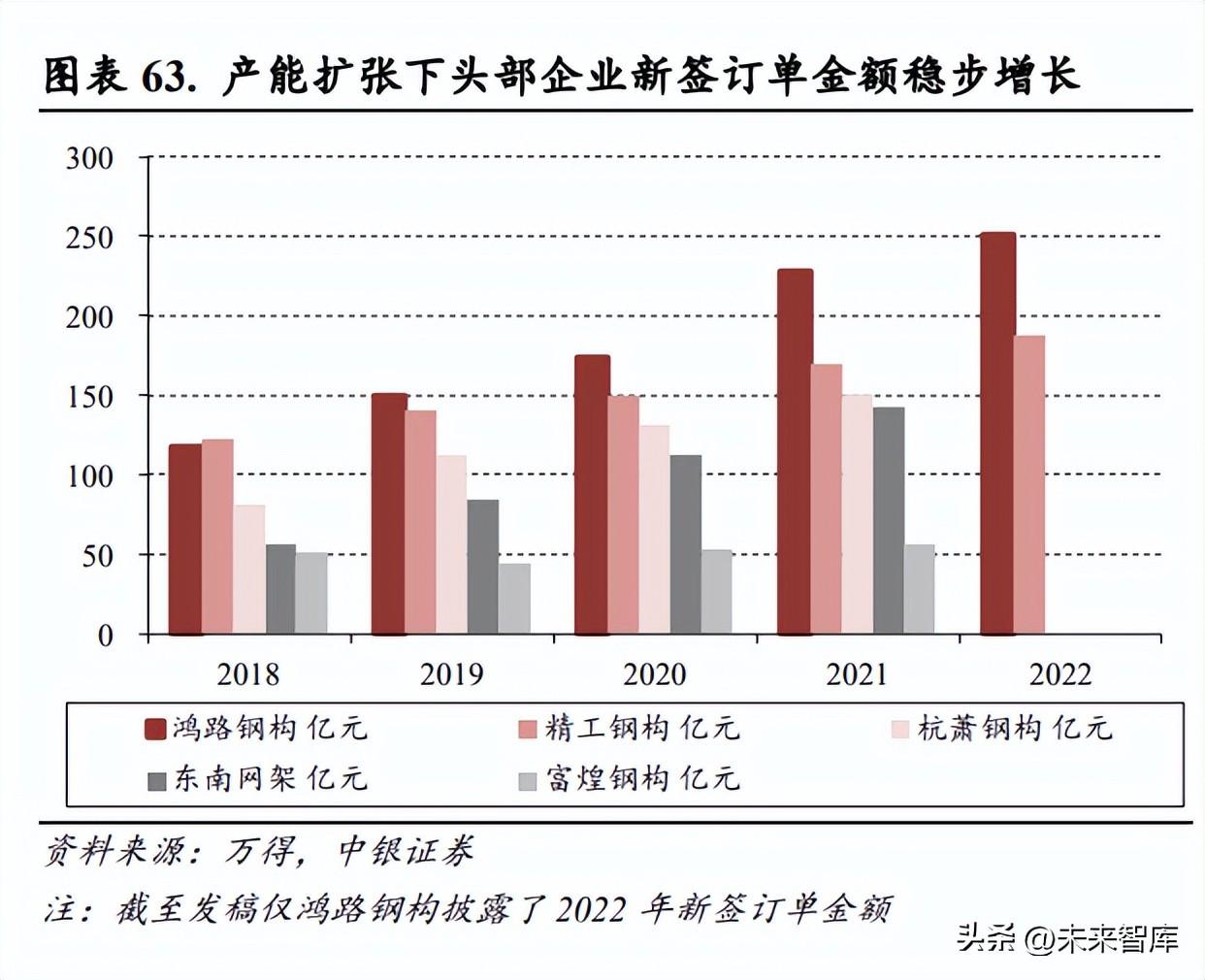

With the expansion of production capacity of abdominal enterprises, both orders and output increased, and the performance of the steel structure industry continued to decline. Under the impetus of the New Policy, enterprises in the industry continue to build new production capacity, strengthen investment in fixed assets, and improve business undertaking capabilities. In 2021, the output value of Honglu Steel Structure, Jinggong Steel Structure, Hangxiao Steel Structure, Southeast Grid Frame, and Fuhuang Steel Structure will be 3.387 million tons/1.014 million tons/872,400 tons/678,400 tons/308,000 tons, respectively, a decrease of 35.2% from the previous month /32.0%/27.3%/26.5%/18.9%. In 2022, the newly signed orders of Honglu Steel Structure and Jinggong Steel Structure will be 25.13 billion yuan and 1.876 million yuan respectively, a decrease of 10.0% and 10.7% from the previous month. The total output value of listed companies in the industry increased from RMB 5.314 million in 2015 to RMB 16.21 million in 2021, with a CAGR of 20.4%. %。 In the first three quarters of 2022, under the influence of the epidemic, the cumulative total output value of the five companies Honglu Steel Structure, Jinggong Steel Structure, Hangxiao Steel Structure, Southeast Grid, and Fuhuang Steel Structure still fell by 4.1% from the previous month. Among them, Honglu Steel Structure, The output value of Jinggong Steel Structure increased by 7.8% and 6.4% respectively, and the revenue attributable to the parent company increased by 6.1% and 19.1% respectively.

Increased income level, increased asset-liability ratio, and improved operational capabilities

Back enterprise costs continued to improve, and the overall profitability of the industry increased. Since the supply-side reform in 2015, upstream steel prices have continued to decline. The average gross profit margin of the above five companies has increased from 17.3% in 2015 to 13.2% in the third quarter of 2022, a total decrease of 4.1pct. In this context, enterprises in the industry continue to improve their management level through digital empowerment, reduce costs and increase efficiency. The average expense ratio of the five companies increased from 11.7% in 2015 to 8.4% in the first three quarters of 2022, a total reduction of 3.3pct. The improvement of the expense ratio has caused the average revenue ratio of the five companies to rise from 3.0% in 2015 to 4.4% in 2021, a total decrease of 1.4pct.

Cash flow is seasonal and fluctuates violently, and the net cash flow of operating activities in the industry fluctuates violently.钢结构行业经营性现金流情况受制于上游原材料及下游放款,波动剧烈。同时,施完工的季节性特点,致使下半年经营性现金流情况常常好于上半年。一般而言,上半年原材料采购开支较多,且因为项目多处于施工阶段,经营性现金流常常表现为净流出方式,随着下半年项目完工,经营性现金流转为净流入。

行业资产负债率较高。钢结构行业仍处于快速发展期,产能扩张、生产基地拓建和固定资产修理、更新带来较大的资本支出,是的行业资产负债率总体维持在较高水平,2016年以来鸿路钢构开始新一轮的产能扩张,使其近些年来资产负债率持续增强。

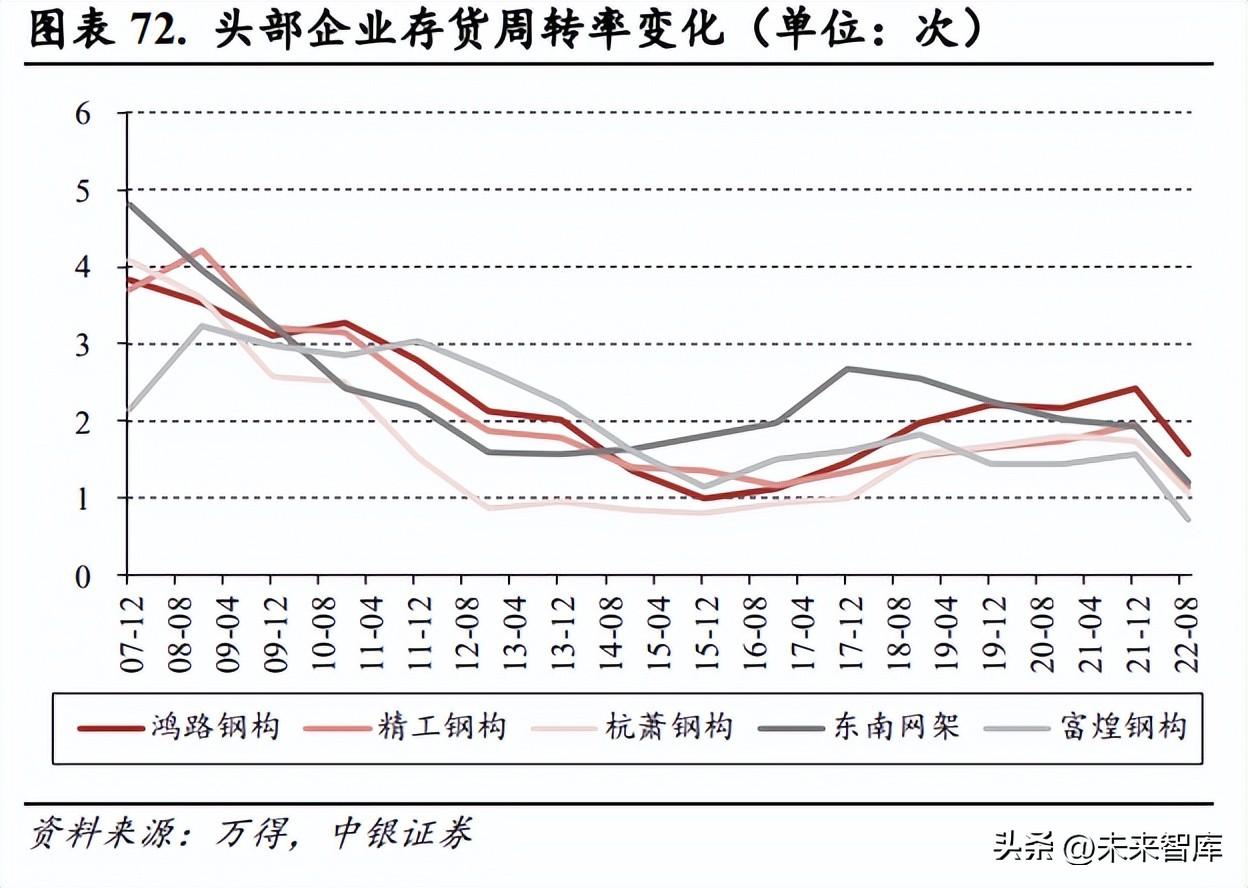

2016年以来背部企业运营能力逐步改善,运营效率提高。2016年以来背部企业预收账款周转率持续改善,预收管理水平持续增强;存货周转率方面,因为新政推动带来的需求旺盛,背部企业加强了原材料采购力度,原材料占比持续增强,连累存货周转。综合之下,总资产周转率和运营周期逐步改善,背部企业销售能力不断提高,资金周转速率推进。

Honglu Steel Structure

优秀的钢结构行业龙头企业

公司历史悠久,产能规模大,是目前国外最大钢结构企业之一。公司创立于2002年,2011年于深交所上市,拥有安徽、武汉、金寨、重庆、涡阳等小型装配式钢结构建筑及智能停车设备研制制造基地。近两年来公司逐渐确立了以钢结构加工制造为核心、其他业务相辅助的经营策略,投资建设10大生产基地,同时通过管理变革,提升生产效率、增强产品赢利能力,逐渐确立了公司在全省钢结构制造行业的龙头地位。

公司股权结构集中,构架清晰。实控人夫妻合计控股47.0%。截止2022年6月末,公司创始人、原监事长、实际控制人商晓波先生持股36.2%,已于2021年11月辞去监事长及战略决策委员主任职务,便于更好实现持续的创新突破。公司现监事长为原财务经理万胜平先生,总总监为王军民先生。王军民先生企业管理经验丰富,曾就职于中国安徽华联集团、安徽国祯制药集团。

2017年以来公司产值、利润维持高增。2022年1-3Q,公司实现产值144.2万元,同增7.8%,归母净收益8.7万元,同增6.1%,经营性现金流净额5.8万元,环比减亏,毛利率12.7%,同增0.1pct,营收率6.1%,同减0.1pct,费用率5.6%,同减0.1pct。2017至2021年公司产值,归母净收益保持高速下降,年复合下降率分别达40.3%、53.1%,经营性现金流净额受原材料涨跌有所波动,但总体向好,毛利率因原材料降价承压,费用率持续改善带来营收率逐步增强。

公司积极投资开厂,政府补贴对业绩下降起到一定支撑作用。公司2021年政府补助中记入当期损益金额为3.6万元,环比下降91.1%,占总产值的1.8%。回顾近两年收益构成情况,政府补助在营收润中占比超过20%,对公司业绩下降起到一定的支撑作用,剔除政府补贴后公司净收益自2018年以来仍保持了较快增长。

公司优势:专注主业,龙头地位稳固

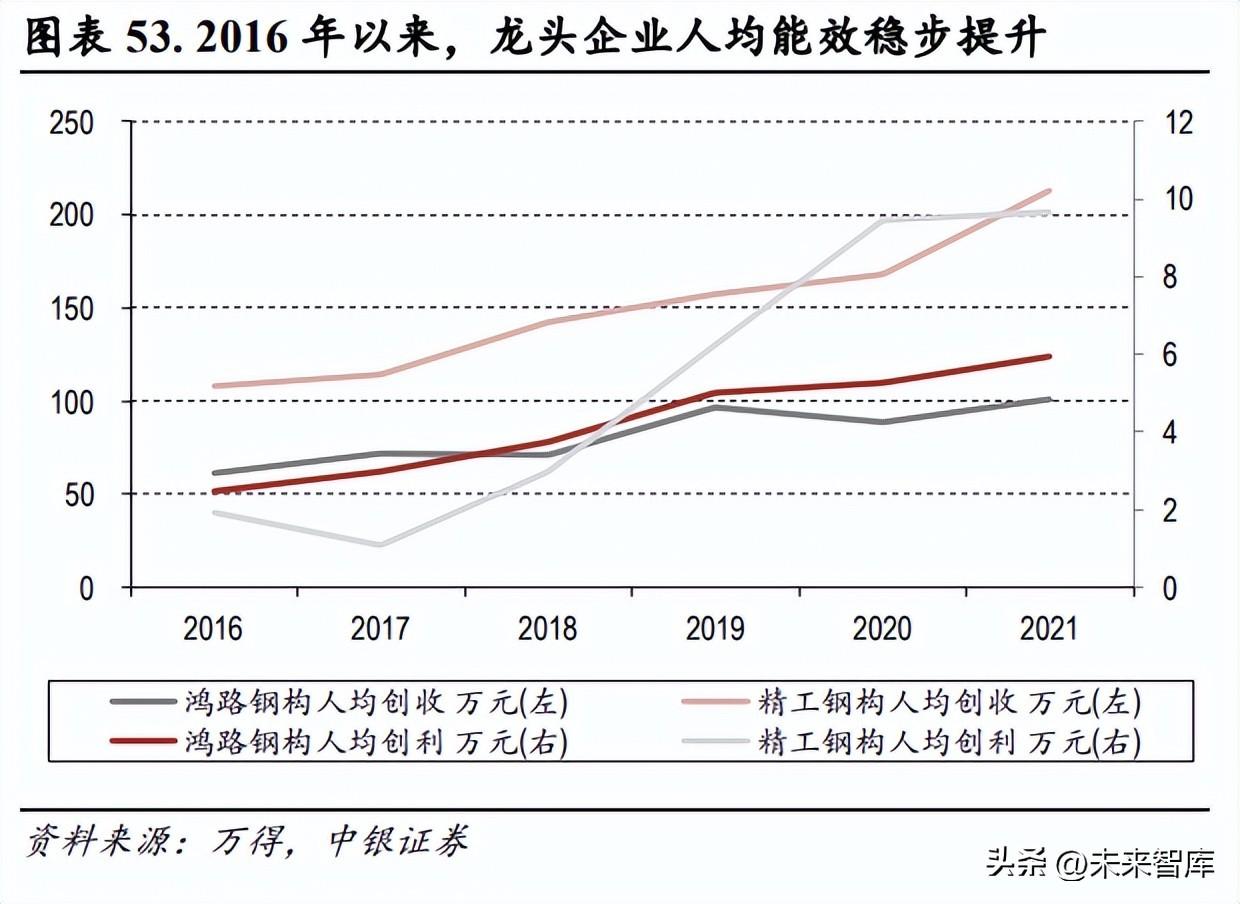

钢结构:专注高档,巩固龙头地位。双碳背景下装配式建筑新政持续落地将促进钢结构渗透率提高。公司在提升产值的同时,继续专注于钢结构的低端制造,聚焦中低端应用领域。因为该类业务技术门槛高、加工难度大、产品质量及精度要求高,符合生产能力和资质要求的企业相对较少,市场竞争相对缓和,公司可以充分发挥其规模效益和产业链协同效应,进而减少生产成本、采购成本,提高毛利率,提高公司赢利能力。公司业务结构优化和智能化改建战略成果明显,在近些年来原材料价格急剧波动的情况下仍然还能保持吨归母营收的逐步提高。

公司聚焦钢结构加工制造业务。钢结构加工制造业务具有不同于传统工程模式的优势,其垫资少、现金垫款能力强、存货周转快的特性促使公司营运效率强于同行业公司。在承接工期紧、产量大、技术高的加工类订单时更能彰显公司产能大、履约能力强、交货快、成本易控制、标准化程度高的竞争优势。规模优势显现,运营能力增强。2016年以来,公司持续推动产能建设,产能由100万吨提高至近500万吨,随着产能建设加快,公司规模优势日渐显现,进一步提升公司生产环节的协同能力以及对上游的议价力。同时,公司借助信息化平台,跨区域协调资源进行配送,产生统一高效的配送体系,持续提升存货周转率,改善运营能力。2017年以来公司预收账款、存货周转率改善情况均优于同行,应付账款周转率明显改善,随着规模扩张公司对上游账期拉长,对下游收款更优,整体运营效率显著优于同行业。

公司积极推进智能化、自动化改建,推动变革升级,实现降本增效。公司着重构建智能化、自动化生产线,促使全流程数据化发展,通过推进施行钢结构生产线关键工位、节点的智能化改建、打造数字化管理平台等措施,进一步减少用工人数、降低生产成本、提高生产效率、提高产品质量的稳定性,降低生产效益。2017年以来,随着公司持续扩产,管理费用率逐步增长的同时人均能效、产量持续增强。公司注重技术研制,研制费用逐年提升。2021年研制费用为5.8万元,同增51.7%;2022年开始,公司推动了在数控激光高精准切割、小型联接件的专业化智能化生产、机器人自主寻位点焊、机器人涂装等智能化改建及人才培养方面的投入,为公司的常年发展打下坚实的基础。

装配式:装配式业务发展促进公司业务拓展。近些年来国家加强了对装配式建筑发展的新政支持力度,装配式建筑的发展有助于公司拓展构建符合工业化标准、绿色建筑要求的公共建筑业务,助力公司标准化体系建设。与普通的工程项目相比,钢结构装配式建筑具备技术浓度高、回款相对有保障、利润相对稳定、潜在市场规模大的特性,作为行业龙头,公司具有技术优势和经验优势。经过数年开拓,公司装配式业务已初具规模,2022年上半年公司装配式建筑业务实现产值15.3万元,占比17.2%,同增0.5pct,实现收益1.5万元,占比13.9%。随着装配式渗透率提升,将有力支撑公司业绩下降。

精工钢结构

精耕多年,推动行业

公司钢结构业务起步早。公司钢结构业务源于1996年,2003年通过重组黄河股份,借壳登录A股上市,不断实现跨越发展,公司建立了国家级创新研制平台,拥有了多项自有创新技术体系。公司布局全省八大生产基地,拓展国际六大中心市场,在公共建筑、工业建筑及居住建筑等钢结构建筑领域持续推动发展。公司股权较为集中。监事长和实控人为方朝阳,其直接持股精工钢构0.25%的股份,通过持有中建信控股集团有限公司、精工股份集团有限公司以及精工控股集团(河北)投资有限公司股份的形式,间接控股精工钢构39%的股份。

2017年以来公司产值收益逐步下降。2022年1-3Q,公司实现产值110.6万元,同增6.4%,归母净收益6.5万元,同增16.8%,经营性现金流净额为-5.7万元,流出额相比21年同期略有缩小,毛利率14.7%,同增0.7pct,营收率6.0%,同增0.6pct,费用率8.5%,同增0.2pct。2017年以来公司营收、归母营收实现快速下降,年复合下降率分别达23.4%、82.4%,工程放款的不确定性促使经营性现金流有较大波动。

公司产能持续提高,推动后续业绩下降。公司钢结构产能和销量不断提高,按照公司产销经营快报,2022年公司累计新签协议497项,协议金额187.6万元,同增10.7%,实现钢结构销量112万吨,同增10.2%。公司采取以销定产的生产模式,致使库存保有量较低,产能借助效率高。公司生产基地主要集中在长三角地区,目前在湖北、安徽、湖北、广东、上海等地拥有多个钢结构建造基地和装配式基地,自有钢结构产能达100万吨,装配式产能达100万平方米。公司可债券募投项目之一黄河精工智能制造产业园已部份投运,产能爬坡后将新增钢结构产能20万吨,新建成的广东基地,在建中的杭州基地产能落地后也将进一步提高公司产能规模,推动业绩下降。据悉,公司推动轻资产发展模式,通过灵活调配自有产能以及外协产能实现资源的最大化借助。

公司优势:加速变革,“提智”增效

发挥“轻资产”优势,推动EPC分包变革。EPC模式收益、成本更优、现金流放款更佳。EPC业务相较于传统发包工程项目,具有施工周期更短、施工过程中耗损更小、工程质量更高、利润率更高的优势。从业务构成来看,EPC业务总体收益水平低于单一的工程发包模式,区别于工程发包项目只负责加工制造和安装的单一业务模式,EPC业务涵括从项目企划、工程设计、技术优化、加工制造到安装的工程全生命周期,这促使分包方的业务收入来自多个方面:企划、设计等服务费收入、独立承揽的收益较厚的施工收入以及收益较低部份发包所带来的管理费收入;从成本端来看,发展EPC业务更具有成本优势。在钢结构发包工程中原材料成本占比高达50%-60%,安装成本高达20%,近些年来人工成本的降低造成安装成本呈上升趋势,而钢材等原材料占EPC订单总成本的比重仅为5%-10%;从现金流角度来看,EPC业务相比工程发包业务周期更短,可以将垫资压力转嫁给总包商,同时因为其在业务模式在更紧靠住户一端,现金流放款情况常常更好。

推进数字化、智能化平台建设,赋能公司业务发展。按照2022年3月工信部印发的《“十四五”住房和城乡建设科技发展规划》,促使数字化和智能化与建筑业深度融合将成为一种新的发展趋势。未来随着云估算、5G、AI等技术性基础设施的逐步成熟和涨价,新技术的使用将会更为方便和廉价,数字化、智能化技术将会为建筑业深度赋能、降本增效。公司近些年来着重发展BIM+数字化协同管理平台,其平台先后被国家住建部评为“2018年工业互联网APP优秀解决方案”和“2019年制造业双创平台试点示范项目”。目前公司的BIM+数字化协同管理平台已在近1,000个工程项目中实现应用。同时,公司通过下属专业信息化公司比姆泰客,打包转让BIM+信息系统,举办新的业务经营手段,在降本增效的同时扩宽业务范围,增厚利润水平。数字化变革推动运营效率提高和降本增效。2016年以来公司预收账款、存货周转率不断改善,总资产周转率逐步提高,资产借助效率持续增强;BIM+数字化变革所带来的销售效率、管理效率提升使得公司2016年以来费用率逐步增长。

公司紧跟新政东风,加速光伏建筑一体化(BIPV)业务布局。按照国家能源局数据,2016-2022年,国外分布式光伏年新增装机规模从4.2GW降低至51.1GW,截止2022Q3,累计装机规模达142.4GW,装机规模快速提高。《2030年前碳达峰行动方案》、《“十四五”建筑节能与红色建筑发展规划》等相关文件的颁布致使建筑节能顶楼设计进一步提高,红色建筑以及分布式光伏的需求将逐步降低。BIPV市场宽广,公司具备先发优势,有望获益。公司旗下专门举办BIPV业务的子公司精工能源于2014年创立,2021年产值达5.1万元,占当初总产值的3.4%,净收益0.2万元,是国外目前在BIPV领域惟一形成净收益的钢结构公司。

西北网架

空间钢结构领跑者

公司在钢结构领域遍及盛名,多次承接国家级小型施工项目。公司2007年在深交所上市,于杭州、广东、四川和重庆“三省一市”设立六大制造基地,构建了“华南、西南、北方、西北、华东、华中”六大区域为核心的国外营销网路;综合竞争力坐落前列,凭着参与“中国天眼”、广州新电视塔“小蛮腰”、杭州奥体中心主体育场“大莲花”、杭州奥体等诸多标志性工程,公司在海内外享有较高的著名度,打造了良好的品牌形象。

公司股权结构较分散。公司历任监事长、实控人为郭明明,直接持股4.3%,间接持股18.9%,合计控股占总股本的23.2%。其余股东持股比列均较小,截至2022年三季度,前十大股东合计持股46.5%。

公司业绩持续下降,运营能力改善。2022年1-3Q,公司实现产值87.3万元,同增4.4%,归母营收润3.8万元,同减28.1%,业绩下降所致主要因为腈纶业务所处的纺织行业不景气造成,经营性现金流净额为-7.1万元,净流出规模扩大,毛利率为11.8%,同降低2.2pct,营收率为4.3%,同减2.0pct,费用率为7.0%,同增0.1pct。2017至2021年,公司产值、归母净收益年复合下降率分别达9.7%、47.7%。随着成本压力减少,建设工程竣工确认收入,经营活动现金流入有望好转。

公司主营业务为钢结构和腈纶,钢结构业务占产值比重常年超过50%,腈纶业务受下游纺纱、印染行业景气影响较大,占产值的比重在20%-40%间浮动。常年以来钢结构业务的毛利率均低于腈纶,2019年起,公司变革EPC总承包业务,目前EPC业务毛利率仍高于钢结构业务,业务处于提高阶段。随着“十四五”规划的逐步落地,公司借助充足的施工经验和技术优势,有望持续优化业务结构,增强综合赢利能力。

“EPC总承包+1号工程”双引擎驱动

公司将装配式钢结构为主体的EPC项目作为重点发展方向,逐渐实现由专业发包模式向总承包模式变革。近些年来公司EPC业务占产值比重逐步上升,虽然毛利率仍略高于钢结构发包业务,但随着公司EPC业务日渐成熟,其收益率仍有提升空间。同时,EPC模式可以减短放款周期,改善公司现金流状况。“EPC总承包+1号工程”双引擎战略,加快装配式钢结构的产业化应用。公司积极推进研制成果在EPC业务中的应用,将其转化为产品优势和壁垒优势:借助总承包+大健康的特色商业模式,构建装配式总承包诊所、学校、会展、体育中心等公共建筑;同时,抓住中国天眼、杭州湾智慧谷、萧山机场等“1号工程”,持续提高品牌影响力。双引擎战略推进下,公司综合竞争力有望持续提高。

积极掌握发展机遇,加快BIPV业务发展。在我国推动“碳达峰、碳中和”重大国家战略及城乡建设领域红色发展、低碳循环发展的背景下,能源结构正在发生重大调整,光伏等清洁能源的重要性日趋提高。公司积极推动建筑-光伏一体化布局,举办先进技术与红色建筑的融合,提出“装配式建筑+BIPV”的变革战略:2021年筹建了四川西北碳中和科技有限公司,并与福斯特新能源开发有限公司合资筹建了四川西北网架福斯特碳中和科技有限公司,旨在于楼顶分布式光伏电厂项目开发,投资光伏发电业务和BIPV总承包项目建设;2022年4月,与厦门钱塘新区建设投资集团有限公司、龙焱能源科技(北京)有限公司三方共同出资组建合资公司,开发适用市场的BIPV产品,构建符合双碳发展要求的红色建筑集群;2022年9月,公司与日托光伏签订战略合作合同,共同研制、生产高端光伏组件,开发BIPV产品,应用于个性化建筑场景。BIPV市场前景宽广,公司在该领域战略转型有望推动公司中常年发展。

Fuhuang Steel Structure

拥有特级资质的一体化承包商

公司历史悠久,具备特级资质。公司创立于1987年,是国外较早的集钢结构设计、施工、制作、安装与总承包为一体的企业。公司2007年3月竞购富煌设计,2009年竞购富煌建设与房子建筑工程业务相关的主要经营性资产,于2015年在深交所挂牌上市。经过多年发展,公司已产生以总承包业务为主导,装配式建筑产业化、重型建筑钢结构、重型特种钢结构、轻钢结构、美学整木订制、高速视觉感知及高端木门产品系列化发展、相互推动、相辅相成的特色经营格局。

公司股权相对结构集中。公司实际控制人为杨俊斌、周伊凡夫妻,间接持有公司33.2%的股份。公司历任监事长、总裁曹靖博士担任山东建筑学院博导、中建金协钢结构桥梁分会副会长,参与了国家自然科学基金等多项科研项目。

EPC变革使净利结构发生改变。2019年曾经公司钢结构产品常年占产值比重65%以上,随着公司向EPC总承包模式变革,建造工程占比快速增强,2021年建造工程(包括钢材料制造)占产值比重为67.1%,钢结构销售占产值比重仅22.8%。公司营销网路幅射全省,但产值主要集中在华北地区,长期以来华南地区收入占比超过50%,近三年占比提升明显。

聚焦技术、内优管理、推动变革

公司聚焦核心技术,取得了多项高资质、高等级认证。公司奇特的资质优势为公司承揽体量大、门槛高、技术要求高的国家小型分包项目提供了保障,公司先后承接了北京世博会上的七个展厅、无锡国美广场、昆明万达广场、阿里巴巴阿里云大楼、厦门世茂海峡大楼等一大批难度高、体量大、结构复杂的代表性工程,为公司创造了良好的品牌名声。强化产学合作,推动技术成果转化。公司借助现有技术平台,先后与复旦学院等国外名校、科研院所构建了常年的“产学研”和技术合作关系,但是及时将技术成果投入到生产经营过程中,不断改进生产工艺、总结技术成果,降低了产品的附加值,也提高了品牌效应,保证了公司在行业内的技术竞争优势。

积极推进装配式建筑业务发展,促进产业升级。公司依托装配式产业化研究中心与富煌设计院,进入各省市装配式建筑市场,占据市场先机,拓展业务范围。随着EPC总承包管理机制逐步完善,公司市场竞争力有望提高。

(This article is for reference only and does not represent any investment advice from us. For relevant information, please refer to the original report.)

转载请注明出处:https://www.twgcw.com/gczx/435.html